The first week of 2026 brought investors a distinctly unromantic reminder: As the macroeconomic narrative shifts from “growth and inflation” to “institutional risk and governance risk,” performance isn’t any longer about whose story sounds best, but reasonably about which assets appear most independent under stress.

The relative strength of gold and silver together with the relative weakness of BTC and ETH reflects this revaluation. Hard assets are competing for an “independence premium,” while large crypto assets are increasingly trading like dollar risks with high volatility. This is just not to say that crypto has lost its long-term utility.

In the present context, the market is concentrated on three questions: What are you willing to accept? Who is the marginal buyer? Which risk area do you belong to inside a portfolio? On these points, the gap between precious metals and crypto is growing.

USD-denominated leverage and “institutional risk”

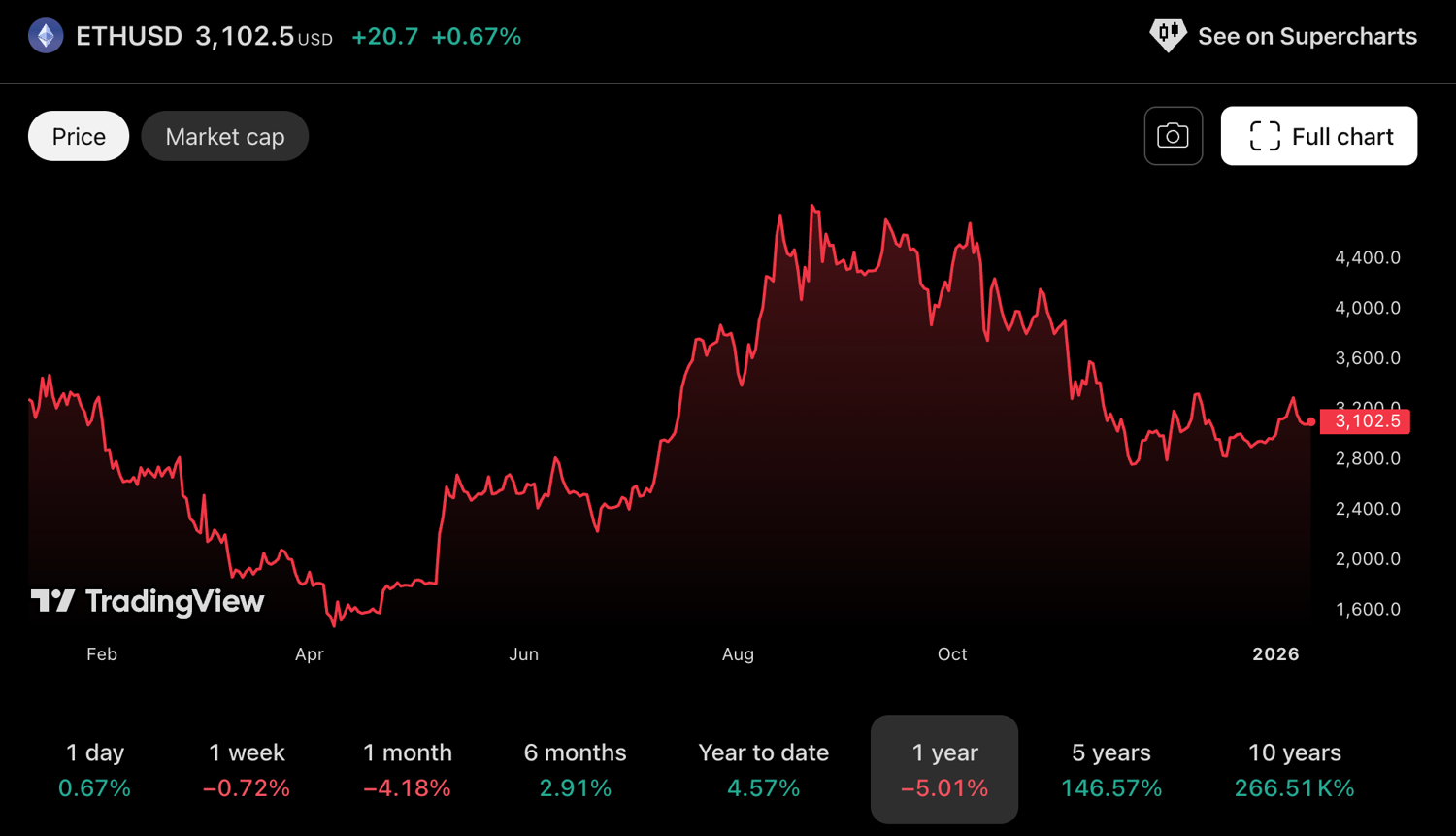

A fast look back at Bitcoin over the past 12 months helps. During the “Liberation Day” rally last April, BTC initially stabilized, then recovered, reaching a brand new high of $126,000 six months later. The “digital gold” narrative was vital, but the actual afterburner was USD-settled derivatives.

From March to October 2025, open interest in BTC Delta 1 contracts increased from about $46 billion to over $92 billion, giving BTC strong leverage and helping it outperform gold within the short term. After the height, extensive crypto deleveraging and changing institutional expectations pushed BTC right into a sustained decline; Gold, however, continued to rise.

Source: Tradingview

One detail is vital: As USDT/USDC and other stablecoins have grow to be established, USD-denominated leverage (not coin margin leverage) has increasingly driven the marginal movement.

As exposure occurs through more standardized, more leveraged channels – exchanges, perps, structured products – the behavior becomes more “portfolio-like”: add risk increase, reduce as a part of a risk budget reduction.

Whether it’s USD pricing, USD collateral, or US yield curve-based cross-asset hedging, BTC easily integrates into the identical USD-based risk framework. So when dollar liquidity becomes tight, regardless of the trigger, BTC is usually one in all the primary to feel the consequences of de-risking.

Source: Coinglass

In other words, the market hasn’t suddenly “stopped believing in digital gold.” BTC is increasingly seen as a tradable macro factor – more aligned with the dollar beta with high volatility than as a store of value outside the system.

What is being sold is less spot BTC and more USD denominated BTC exposure. Once leverage is large enough for capital flows to dominate fundamentals, BTC behaves like a classic risk asset and is sensitive to liquidity, real rates of interest and financial policy.

Gold is different – no less than for now. Its price continues to be primarily determined by spot supply and demand reasonably than leverage. It also retains monetary properties and is widely accepted as security: a form of offshore hard currency. This makes it one in all the few assets that is just not directly determined by on a regular basis fiscal and monetary conditions.

This is vital on this environment. The Trump administration has increased macroeconomic and political uncertainty (consider events in Venezuela and Minnesota). For global investors, holding dollar assets and dollar leverage now not seems like “parking the ship in a protected harbor”; Even at the extent of pricing and settlement, it presents institutional risk that’s harder to model and might challenge the predictability of market rules.

Therefore, reducing the synthetic risk of US policy is a wise step. Assets which can be more tied to the dollar system and behave like risk assets under stress are likely to be cut first. Conversely, assets which can be more clearly separated from government bonds and fewer depending on “permitted” financial infrastructure appear more favorable in the identical risk model.

This is a headwind for crypto and a tailwind for precious metals: independence is the purpose. When markets fear shifting political boundaries and weaker rule predictability, gold (and other precious metals) deserve the next independence premium.

Since 2025, this premium has been more visible. A pleasant comparison is silver with ETH. In the general public imagination, ETH was once often known as “digital silver” (and within the PoW era it probably was). Both were viewed as smaller-cap investments which can be more vulnerable to squeezes and leveraged moves.

But ETH, an equity-like asset closely tied to the dollar system, has long since lost any independence premium. Silver, as one in all the historic “offshore hard currencies,” has not done this. Investors are clearly willing to pay for this independence.

The “Dollar Beta Discount”

USD-denominated leverage can also be a key reason why options markets remain structurally bearish on BTC and ETH. The “New Year effect” briefly lifted each values in the primary few sessions, but didn’t change the longer-term positioning.

As investors have continued to cost in rising institutional risks in dollar assets over the past month, the longer-term bearish trend in BTC and ETH has continued to strengthen. Until the share of USD leverage declines significantly, “independence under institutional uncertainty” is prone to remain the market’s organizing principle.

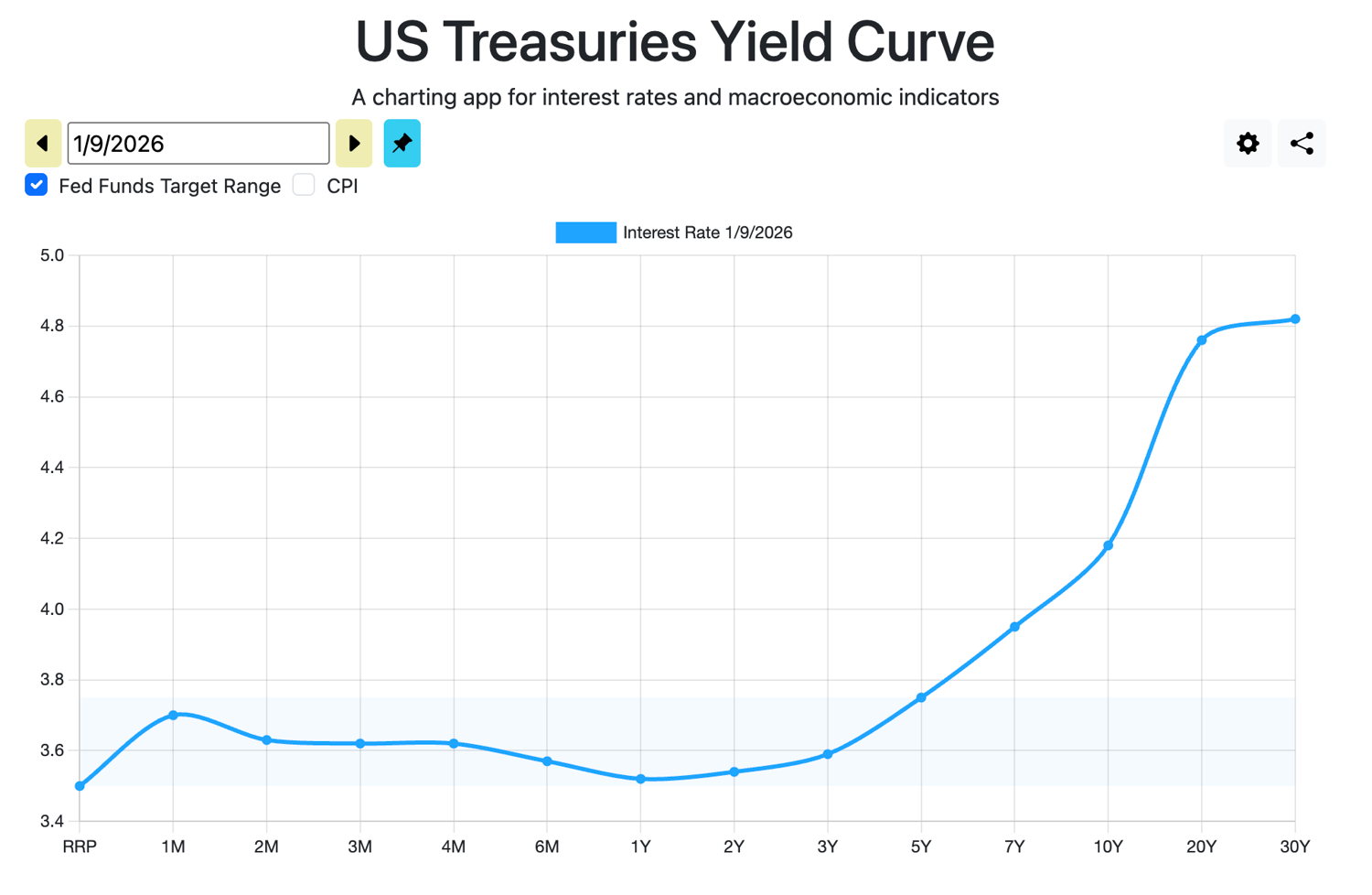

At the identical time, as valuation expectations for dollar-pegged assets are lowered, investors are demanding higher risk premiums. The yield on 10-year government bonds continues to be at a high level of around 4.2%. Because the Treasury and Fed are unable to totally dictate pricing for a 10-year term, this level increases the hurdle rate for dangerous assets.

But the “dollar beta discount” related to USD leverage reduces the implied forward returns for BTC and ETH (to five.06% and three.93%, respectively). BTC May Still Look Bearable; ETH, let alone. ETH due to this fact has a bigger dollar beta discount: returns are uncompetitive and upside convexity is restricted. None of this affects Ethereum's long-term potential – nevertheless it does change allocation decisions over a one-year time horizon.

Cryptocurrencies can in fact bounce back: when financial conditions ease, political uncertainty subsides, or the market returns to growth and liquidity, high volatility assets will naturally respond. However, macro investors give attention to taxonomy. When institutional uncertainty prevails, cryptocurrencies act like risk assets; Precious metals are traded more like “exceptionalism assets.”

This is the message for early 2026: crypto has not “failed” – it has simply lost its price place as an independent asset on this macro regime in the meanwhile.

Disclaimer: The information provided here doesn’t constitute investment advice, financial advice, trading advice or another advice and mustn’t be treated as such. All content listed below is for informational purposes only.

The post BloFin Research Analysis: A Shift in Capital Preference From Bitcoin to Gold appeared first on BeInCrypto.

Article source: beincrypto.com

The post BloFin Research Analysis: A Shift in Capital Preference From Bitcoin to Gold appeared first on Crypto Adventure.